Copy to clipboard

Copy to clipboard

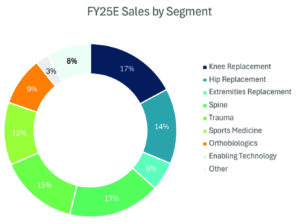

The joint replacement segment generated $23.9 billion in worldwide sales in 2025, comprising 37% of the orthopedic market. Knee replacement accounts for nearly half of joint replacement sales and is roughly equal to the size of the spine market, as shown in Exhibit 1.

Exhibit 1

Here we’ll look at the top-performing companies in joint replacement, the impact of enabling technology on the segment, major developments in the competitive landscape, and two companies to watch.

Lucrative Opportunities Available for Disruptive Challengers

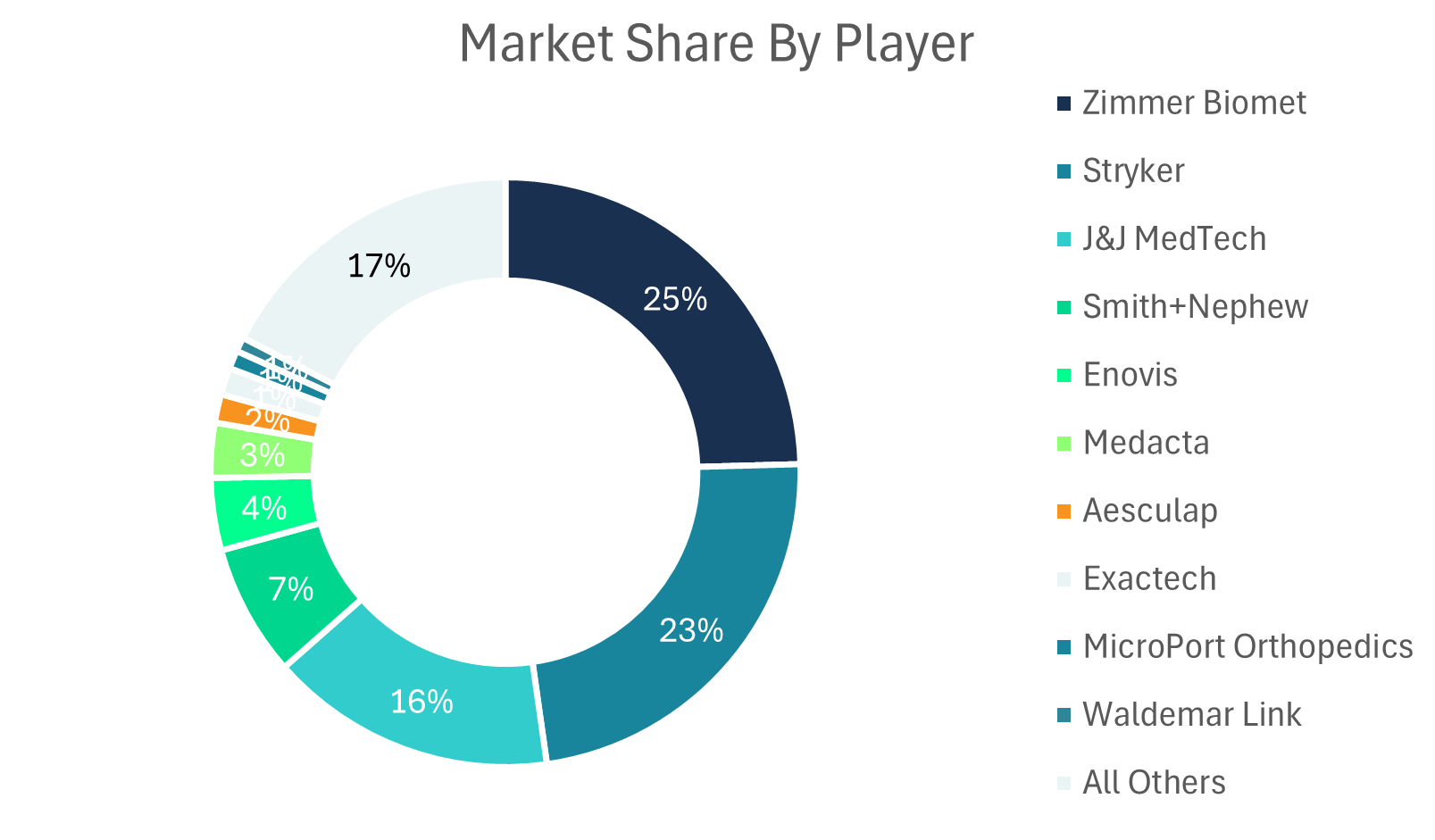

The joint replacement market remains the domain of orthopedics’ largest companies. The quartet of Big Four companies in the market — Zimmer Biomet, Stryker, J&J MedTech and Smith+Nephew — controls 71% of worldwide joint replacement sales, as seen in Exhibit 2.

The Big Four is more accurately the Big Three, as Smith+Nephew holds less than half the share of its nearest competitor, with companies like Enovis and Medacta closing the gap and nearing the $1 billion threshold for joint replacement.

Exhibit 2

I expect Enovis and Medacta to continue narrowing the margins, but it’s worth remembering just how big those gaps are. For joint replacement, Enovis is $800 million behind Smith+Nephew, which has less than half the revenue of the next player up, J&J MedTech. But you don’t need massive share jumps to make money in joint replacement. One percent of market share is worth about $240 million in sales.

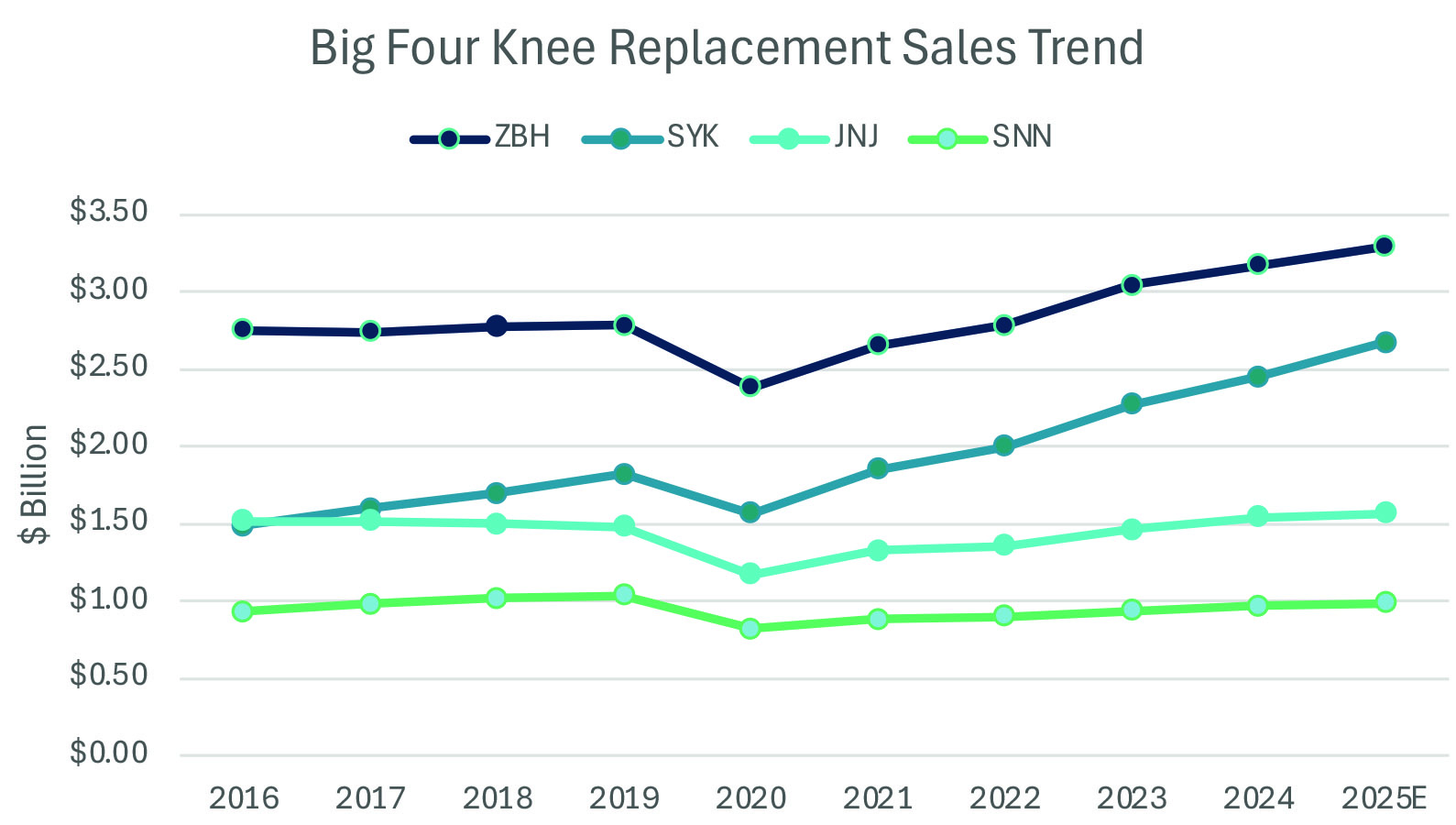

Knee replacement, in particular, has seen large shifts in market share as robotics has changed the competitive landscape of orthopedics. According to our estimates, Zimmer Biomet controlled over 32% of the knee replacement market in 2016. Since then, the company has lost about 3% share.

Zimmer Biomet isn’t alone. J&J MedTech lost nearly 4% share over that time frame, while Smith+Nephew dropped 2%. For context, 1% market share in knee replacement was worth about $110 million in 2025.

Stryker, however, picked up almost 6.5% share over the last decade due in large part to its Mako robotic system. More on that later.

But there’s been some slippage of share from the Big Four. As a group, these companies saw their knee replacement market share erode by 2.3% over the last 10 years as mid-tier companies established themselves in the market. Exhibit 3 highlights the Big Four’s knee replacement revenue over the last 10 years.

Exhibit 3

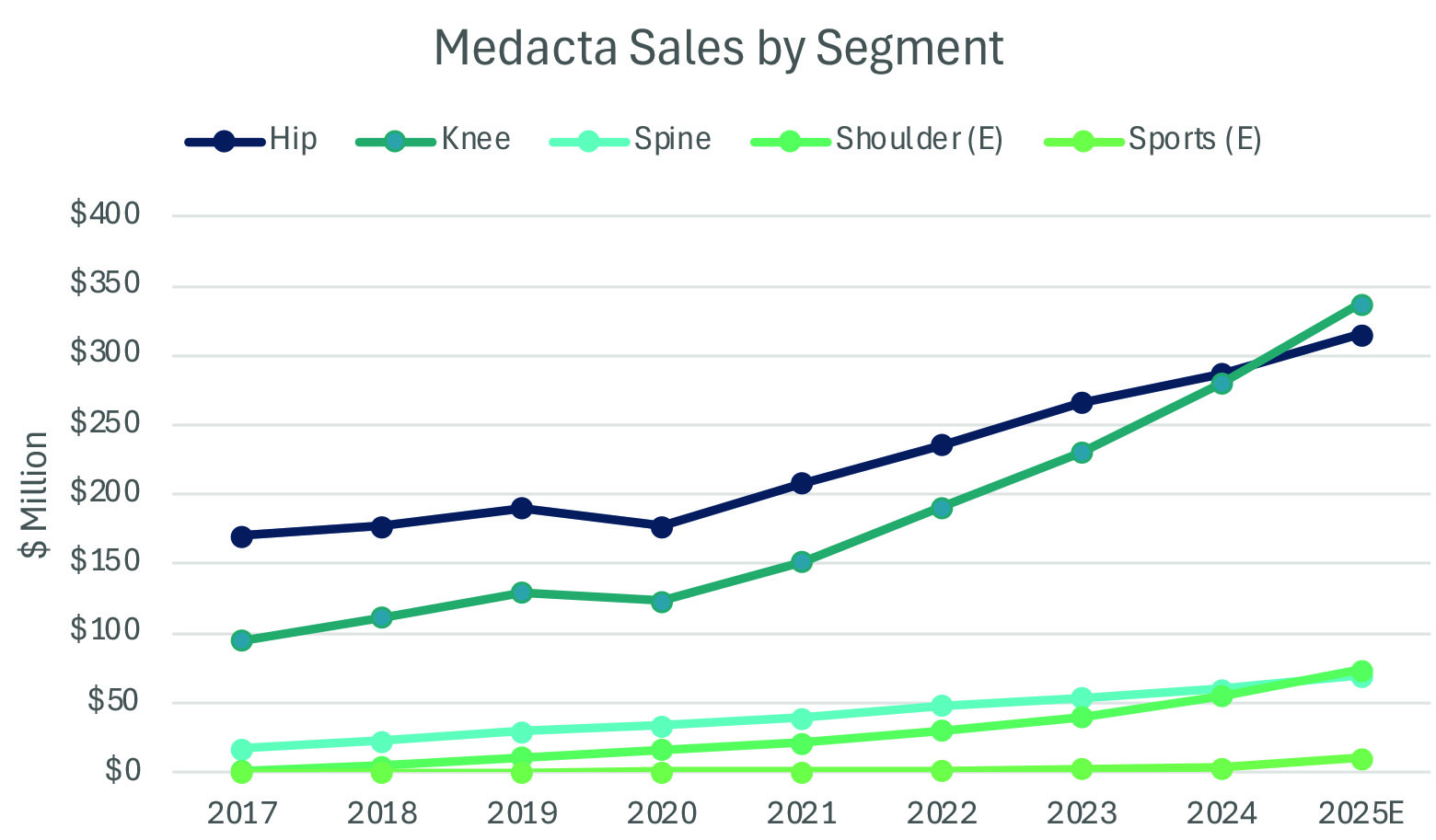

There’s perhaps no better example of a disruptive challenger in knee replacement than Medacta. Its kinematic alignment optimized implant steadily gained market adoption while a robust supply chain helped the company fill voids left by competitors in the wake of the pandemic.

Its knee replacement trend line from 2020 on (shown in Exhibit 4) is about as steep as they come for large orthopedic companies.

I think very highly of Medacta’s culture and approach to the market. Their growth speaks for itself, and I don’t see their trajectory changing any time soon. The biggest challenge for Medacta will be maintaining its current focus and culture as it grows into an extremely large company.

Exhibit 4

Pathway to Technology Leadership

There’s no question that enabling technology has impacted the competitive balance of orthopedics. Even companies that have long taken the wait-and-see approach are redoubling efforts to build out their technology portfolios.

“With respect to enabling tech and robotics, we’ve clearly heard the message that enabling tech is a key part of having a complete global portfolio,” said Enovis CEO Damien McDonald. “We’re examining whether large-format robots are cost-effective solutions and improve patient outcomes, and whether entry into the market at this point is really valid. We’ve got resources dedicated to exploring all the viable pathways.”

Enovis’ conservative approach is a strategically wise decision. Their ARVIS system is very promising and plays well in the ASC, which is a major part of what Enovis wants to do.

The company is evaluating full-size robotics, and it will be interesting to monitor the approach that Enovis takes. They’ll almost certainly need to buy another company that has a system that can be adapted.

While enabling technology in general is a no-brainer, robotics is still a bit of an open question in terms of format and functionality.

Robotics remains underpenetrated among surgeons. According to Zimmer Biomet, 80% of U.S. surgeons don’t use robotics. Internationally, the number is closer to 90%. If those surgeons haven’t adopted large-footprint robots by now, there’s a chance they may never do so.

That’s why Zimmer Biomet believes the pathway to robotics leadership is through optionality. The company has assembled a wide array of technologies over the last several years to meet surgeons where they are.

The newest major addition to Zimmer Biomet’s expansive technology portfolio is Monogram’s autonomous robotic platform.

It’s fair to question the demand for autonomous robotics in the current market, but Zimmer Biomet is confident in the promise of the technology. Not everyone agrees. Stryker said that Mako is already capable of autonomous function, but the company decided not to turn the feature on because there is no demand.

“I’m not going to comment much on competitors and their abilities or lack of abilities,” said Zimmer Biomet CEO Ivan Tornos. “But if they can turn it on, I will recommend that they do. Because this type of technology will change the world of orthopedics.”

One of the major proposed benefits of autonomous robotics is the significant reduction on cognitive load for surgeons. Zimmer Biomet said that its due diligence and surgeon feedback suggest this benefit will be highly disruptive in the market. And for those surgeons who aren’t comfortable ceding that much control, Zimmer Biomet has a bevy of other technology options for them.

The company is banking on its array of technology to help unlock the potential of its knee and hip franchises, especially in the U.S. where its performance has lagged in recent years.

I see the current robotics environment as a defensive measure for the top implant players. For the most part, they’re better at defending existing market share gained through pull-through arrangements than they are at taking share from competitors. Robotics are the moat around the castle.

The big exception, of course, is Stryker. They’ve increased their worldwide knee share by about 6.5% over the last decade, and probably closer to 10% in the U.S., due in large part to their Mako robot.

Remember, orthopedics is a slow-moving industry, even relative to other healthcare sectors. Robotic offerings will improve and evolve while adoption increases incrementally. The timeline of robotic advancement and adoption is probably better measured over careers than quarters.

The Shifting Competitive Landscape

Some interesting joint replacement news came to light in 2025, like Zimmer Biomet’s Breakthrough Device Designation for its iodine-treated hip, Stryker’s clearance for its Incompass Total Ankle or restor3d’s 510(k) for the Identity CR 3DP Total Knee.

But the elephant in the room is J&J MedTech’s announcement that it plans to spin off its orthopedics business within the next two years and bring back the DePuy Synthes name. And while not strictly related to joint replacement, the move promises to create significant disruption through orthopedics.

J&J MedTech’s orthopedics business has a 10-year CAGR of just 0.1%. Looking deeper into the company’s performance over that span, there are plenty of trouble spots. Its spine business got eaten alive, while knee replacement has been unable to find traction. Hip replacement has been better, with a 2.3% CAGR over 10 years.

One bright spot has been the VELYS robotic platform and surrounding ecosystem, which has provided tailwinds for the company in knee replacement, especially outside the U.S. The platform received CE and CA Mark international approvals in mid-2023. By early 2025, VELYS had racked up 110,000 procedures across 30 countries.

DePuy Synthes will likely emerge from this move as a more focused company with a chance to be more competitive. Eventually. But we expect a few hard years ahead, and possible contraction of its share positions in the U.S. and internationally.

Companies to Watch

After a long freeze of IPO activity in orthopedics, Shoulder Innovations was one of the first companies to go public after the recent thaw. The company’s InSet glenoid technology provides the potential for a greater amount of mechanical stability between the implant and the bone, and specifically addresses the rocking horse effect in total shoulder replacement.

The company identified the emergence of ASCs as a key competitive advantage, as its ecosystem is tailor-made for efficiency. Shoulder Innovations CEO Rob Ball previously spoke at OMTEC® and reflected on that advantage.

“The reality is for most implants out in the market, it’s very difficult to change the surgical techniques,” he said. “Sitting down with about eight trays of instruments and seeing which ones we can chuck out of the box and make this smaller footprint tends to be somewhat impossible; you have to go back and reconceive how the implant and the surgical technique are executed.”

restor3d is another company that could make the IPO leap in 2026. The company’s patient-specific approach could be the missing key to improving satisfaction among joint replacement patients.

Investors clearly believe in the company, as it announced a strategic investment partnership with Partners Group. Under the agreement, Partners Group will acquire a significant minority stake in restor3d and provide $65 million of new equity.

An additional $39 million was raised from existing shareholders as part of the transaction.

With improving macroeconomic indicators and a very healthy revenue base, we wouldn’t be surprised to see a substantial initial public offering from restor3d before the end of the year.

The Year Ahead

J&J’s spin-off or Zimmer Biomet’s share losses in 2025 weren’t necessarily surprising, but they are both noteworthy and will drive a lot of the strategic decisions we see this year.

Joint replacement M&A hasn’t been common over the last few years, but I’m interested to see whether large acquisitions or divestitures occur in 2026. Joint replacement is lucrative, but doesn’t have the growth profile to wow investors.

I’ll also be monitoring the rapidly growing patient population, advancements in technology and opportunities to address unmet clinical needs like patient satisfaction in what’s sure to be another eventful year in the joint replacement market.

Mike Evers is Senior Market Analyst at ORTHOWORLD